Evolution (EVO)

Evolution (EVO)

Hi!

Investing outside US? You probably think of China. But how about Sweden? We all know Spotify, Skype, IKEA, even Minecraft. Klarna is one of the hottest upcoming IPOs. Sweden’s fantastic business culture has also allows a company like Evolution to grow rapidly. IMO it’s definitely one of the best investment ideas outside US right now.

This post will be a combination of data and my personal view, so please remember that this is not an investment recommendation of any kind.

I am going in the following order:

Brief history

Business Model

Market

Financials

Stock/Valuation

Risks

Summary

Brief history

The company has been founded in 2006 by Jens von Bahr (Chairman of the Board now and the largest shareholder with 10% skin in the game). They went public in 2015 as Evolution Gaming, both headquartered and listed in Stockholm.

Business Model

1) Overview

Evolution is an online B2B casino supplier focused on the fastest growing segment called “Live Casino” (for example, in poker game there are real dealers with real cards in real studios, but players make decisions online in real time, watching video stream).

They are “picks and shovels” of the industry, offering products for more than 300 customers (gaming operators) around the world. If you are interested in gambling, you probably now such names as: DraftKings, PokerStars, Penn National Gaming or Unibet.

Evolution provides all aspects required for gaming operator - starting from training dealers/game presenters, ending with creating games, streaming them and producing visual effects.

Moreover, gambling also looks a bit different in Asia, the US and Europe. Looks different for big and small providers. And all EVO’s products and services are tailored to the needs of particular customer.

2) How do they make money?

Their typical customer agreement is three years. During that time EVO is charging:

a) commission fees - 10-20% of gross operator’s winnings (customer win = our win)

b) fixed fees for dedicated tables - paid monthly (recurring revenues)

Commission fees are the main source of revenues. I love this model, because they benefit from the growth of their customers, and therefore the market as a whole.

3) Approach

The company is simply obsessed with improving the offer and increasing its advantage over competitors. As their COO, Todd Haushalter, often mentions:

“We spend a lot of time thinking about players we don’t have”

They are introducing more and more new games and take advantage of network effects by increasing the customer base and thus players willing to take part in new challenges (which consequently leads to higher margins). The strategy seems to be working. Not only is the customer base growing, but also user activity.

The best way to keep customers in the game is to have a high level of so-called RTP (Return To Player). In traditional games, such as Blackjack, Evolution has an RTP of more than 99%, while in the company's proprietary titles, the index drops to 95%, because the company has to deduct the costs associated with their production. The RTP of both games is of the highest quality, and the proprietary ones are no less popular because of the lower RTP levels.

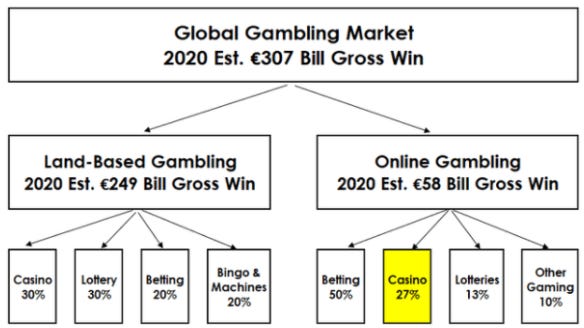

Market

Gambling is a huge market estimated over 300 bn EUR (~350 bn USD). Land-Based segment is still 4x bigger, but Online is closing the gap faster and faster (16’-19’ CAGR 12% vs 2%).

The main market for online casinos is definitely Europe (60% in 20’), with the best internet connectivity. For now. Because Asia (18%) and North America (15%) are getting stronger.

As mentioned before, Live Casino is the fastest growing Online segment (16’-19’ CAGR 32%) and Evolution is leading the way by far, with 50% revenue CAGR 16’-20’.

What are the Online Gambling advantages?

Obviously, as an end customer you can play wherever you are and don't need to inhale tons of cigarette smoke in traditional casino.

Online Gambling is incomparably more scalable than the Land-Based. Thousands of players can play on one table at the same time.

Increasing market regulations attract more online operators. Once you set up in a given region, it's hard to beat you later. At this point I would like to mention that more and more US states are opening up to gambling lately, which paves the way for tens of millions of potential players. Competition among operators is already fierce, but it is known that the vast majority of them will choose Evolution as their service provider :-)

Financials

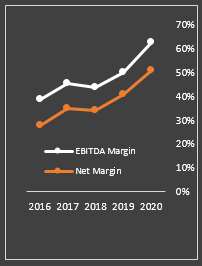

After looking at the EVO business, let’s take a look at the financials, which are just mind-blowing:

65% EBITDA margin? Why not? 50% net margin? No problem.

Maybe its not visible above and I said it before, but I have to remind you that revenue is growing 50% CAGR (16’-20‘).

Their business model is so effective that they can generate 50% FCF/Sales. Can you even imagine?! FCF level is bigger than their revenues from just two years ago!

Debt reduced to zero.

You are looking probably at high level of non-current assets? They are mostly studios all over the world.

Most of their costs are personnel-related and facilities-related.

I don’t like that they are paying dividend already, however I believe that they are just not able to reinvest such amounts on cash. Moreover, I think its more typical for Swedish business culture that you are paying dividend even at growth stage.

In summary, you have to admit - their financials are one of a kind.

Stock/Valuation

It’s pricey, I cannot imagine that such a business would not be.

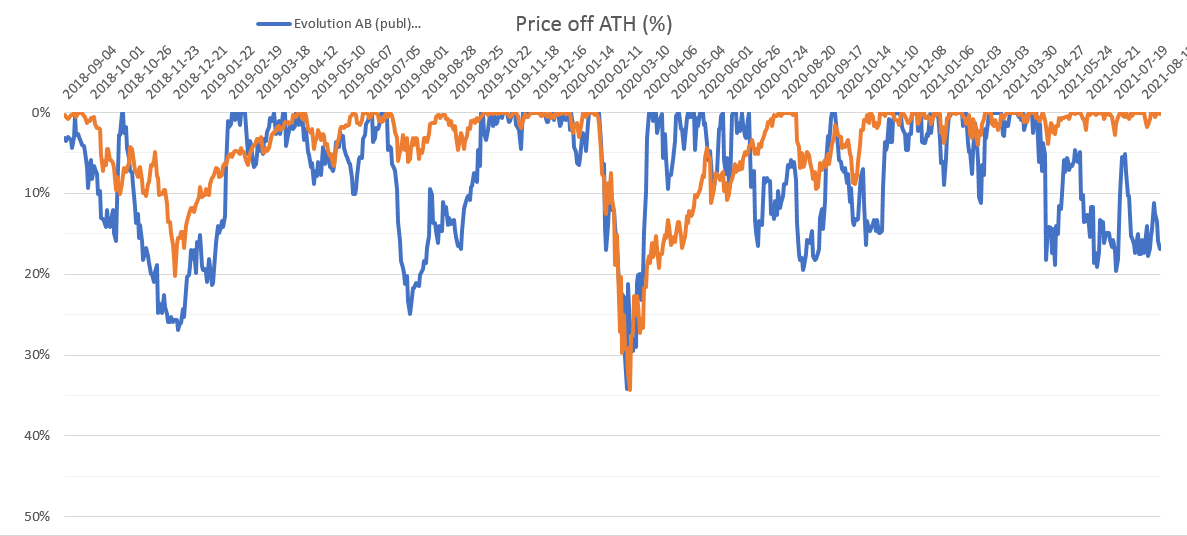

5-year CAGR is 100%, but P/S still under 40 and EV/EBITDA just over 40. Given their rapid increase in margins, stock is definitely followed by business numbers. Of course, there are strong steep dips regularly with such hottness, but the returns are just as quick. For me, every 15-20% dip (as right now) is an excellent point to increase position.

Last time the price formed a solid base around 1350. Any stronger break in either side may determine the condition of the short-term (if someone interested).

Risks

Like any high-growth company, it will not grow at such a pace indefinitely. Any sign of a slowdown can give a sharp shake to the stock price.

Losing famous clients such as DraftKings or Unibet could damage the stock. However, I do not believe that this would harm financials at all and that stock drop would be comparable to Kambi’s - another Swedish B2B gambling provider (though not in casinos, but sports betting) - a 30% drop. Evolution's customer base is incomparably more diversified, and it would take a really large number of customers left to lose its leadership position in the industry.

Just as regulations favor the development of the gambling market so far, they may become its undoing in the future. As mankind grows, awareness of the importance of mental health grows. It is not entirely moral to make money on addicted players, so potentially the authorities may be interested in it. For now, we can only expect such moves in China, but there is always a business risk that the West will also finally become interested in the topic. Although I would say that this is a rather distant future, if at all.

EVO is doing a great job in distancing any competition, but with such juicy returns there will be more and more candidates. Eventually one will succeed. Any sign of a slowdown in the influx of new customers could be a potential red light that the competition is catching up with.

Summary

CEO of Evolution, Martin Carlesund, likes to say it often:

“While barriers to entry are relatively low, the barriers to success are considerably high”

They found a great niche in fast growing market and they are leading by far. Their management is doing amazing job with constant improvements and customer-focused approach. The financial results speak for themselves - Evolution is a great business model with still great opportunities. An additional advantage for me is the Swedish location - a high growth profitable company, which stock is not correlated with American tech, is just pure gold. EVO is one of my highest convictions holdings. I am going to hold for years and watch closely their expansion, especially in the US.

If you liked it, feel free to subscribe for more:

Any feedback will be much appreciated!