Sea Limited (SE)

Hi!

Today I am gonna show you one of my favourite companies, which is well known (at least in Fintwit community) - Sea Limited. It will be combination of data and my personal view, so please remember that this is not an investment recommendation of any kind.

Sea Ltd. was founded in 2009 by Chinese-born Singaporean - Forrest Li, who is still in charge of the company (and holds 25% of all company shares, which made him billionaire in 2019 - just after he was 40 years old).

The company consists of three entities:

1) Garena

It is the oldest one (2009) and it offers in-house made online games in over 130 countries (FreeFire was the most downloaded mobile game in the world (!) for the last two years). But what is more attractive to me: it is also one of the leading esports organizer.

Interest in esports gained a lot of momentum during the pandemic, however this trend has been grown even before. This market offers tremendous opportunities. Just in the last year e-sports revenues hit almost 1 bln $ and according to estimates till 2023 it should grow at least 15% annually, to over 1.6 bln $.

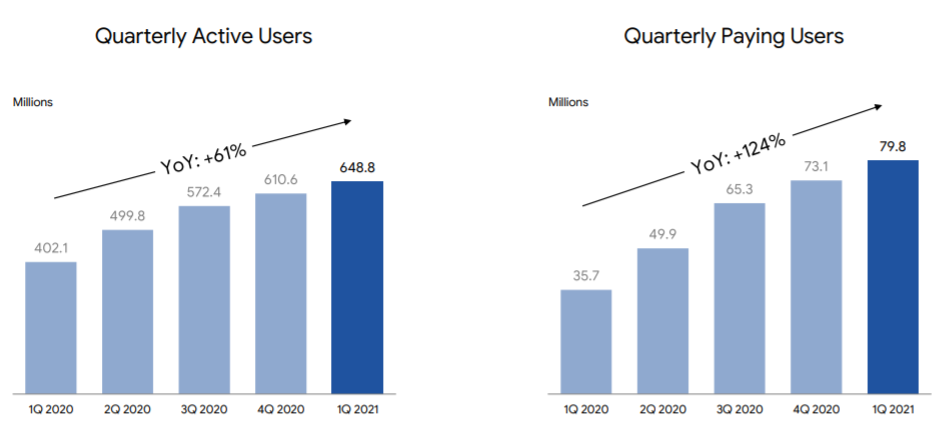

In the 1Q’21 Garena has reached 648.8 mln active users which is 61% more than the year before, but what is more important, paying users grow even two times faster.

2) Shopee

Established in 2015, Shopee is the leading e-commerce platform in Southeast Asia. In 2020 it was visited over 280 mln times, which was more than twice as many as the second best - Lazada (owned by Alibaba).

Again, there has been lot of attention in e-commerce during the pandemic. Total number of internet users in the Southeast Asia has reached already approximately 400 million, which is highly correlated with growing interest in e-commerce solutions. But its not just a pandemic case. As all the tech-like life improvements during this crazy time, momentum in Asian e-commerce platforms are not going to slow down (especially that it was there even before). What is more, the region’s online retail penetration rate is still only 5%, whereas for example in China it is already 32% (a lot of established players there: JD, BABA, PDD). So there is a lot of room to grow.

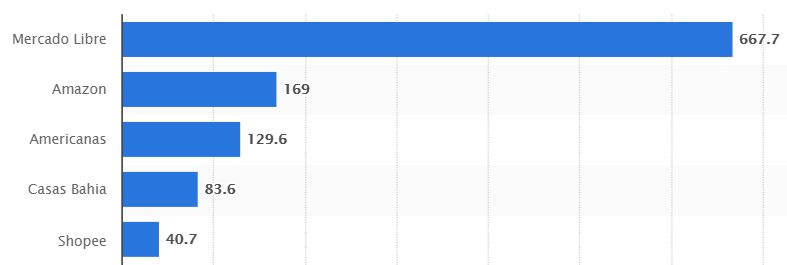

As Southeast Asia remains core market, Shopee is entering Latin America market as well, mainly focusing on the most populated Brazil. It is still early phase here, however, it is already 4th the most visited online marketplace in the continent (according to Statista; data below showed in millions, as of April’21).

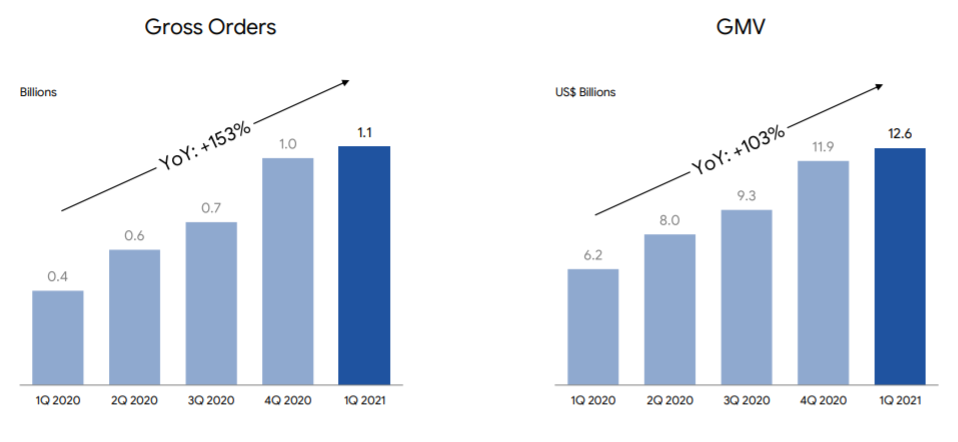

In the 1Q’21 Shopee has reached 1.1 bln orders which is 153% more than the year before, and Gross Merchandise Value (which is total value of merchandise sold through C2C) doubled.

3) SeaMoney

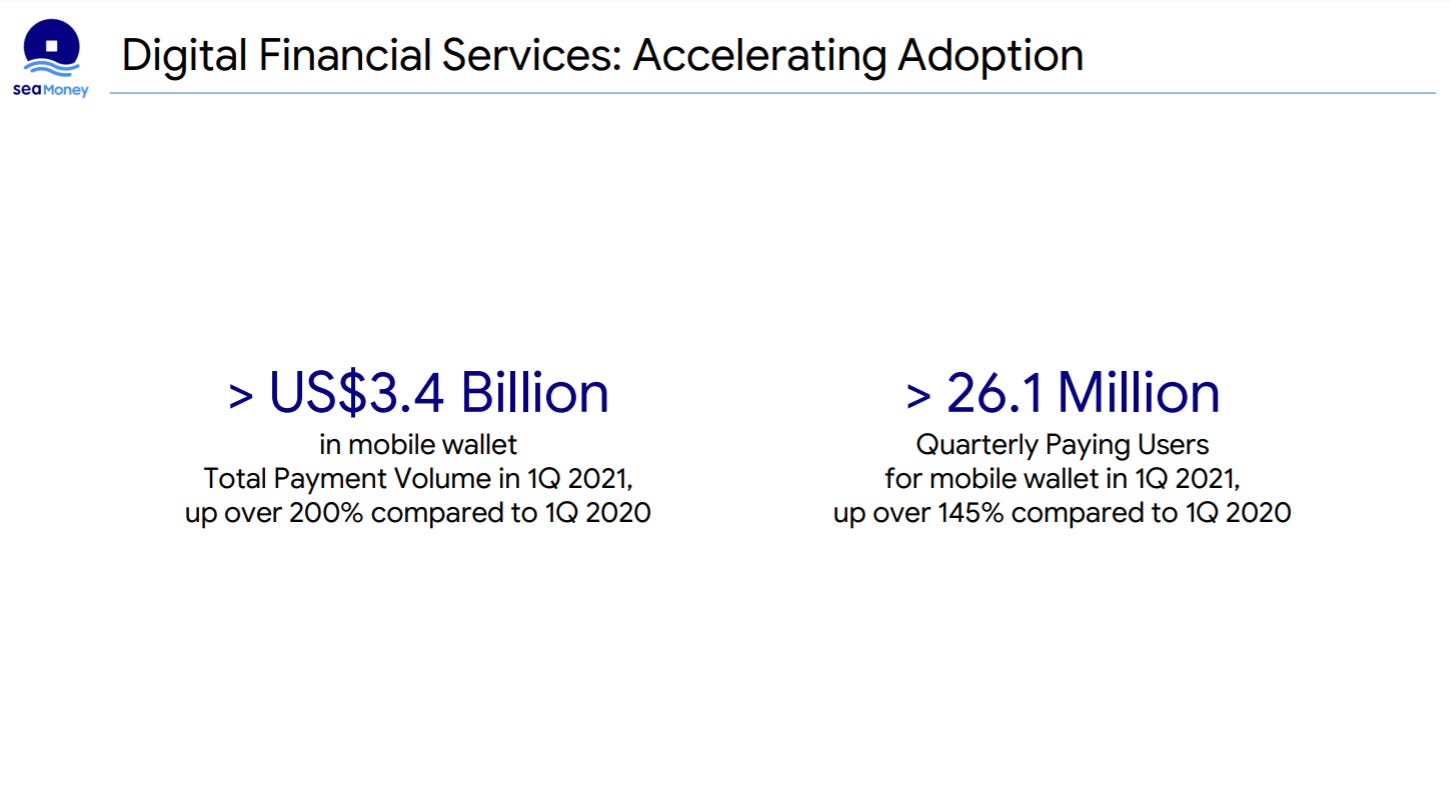

It is the newest Sea’s business and is a digital payments and financial services provider in Southeast Asia. It offers mobile wallet services, payment processing, credit offerings, and other digital financial services/products. There are few brands offered, such as AirPay, ShopeePay or SPayLater. They have already over 26 mln paying users (Q1’21) and 3.4 bln $ in mobile wallets.

———————

What I really like is that all of these three businesses are not just independent entities, but they converge with each other. In short, people can literally buy some gaming-related stuff in Shopee and pay for them via SeaMoney. I think that this makes the whole company so attractive and diversified. And I don’t have to worry about any future headwinds in one of these industries, because the other two are able to fill the gap so well.

Financials

After looking at the SE business, let’s take a look at the financials:

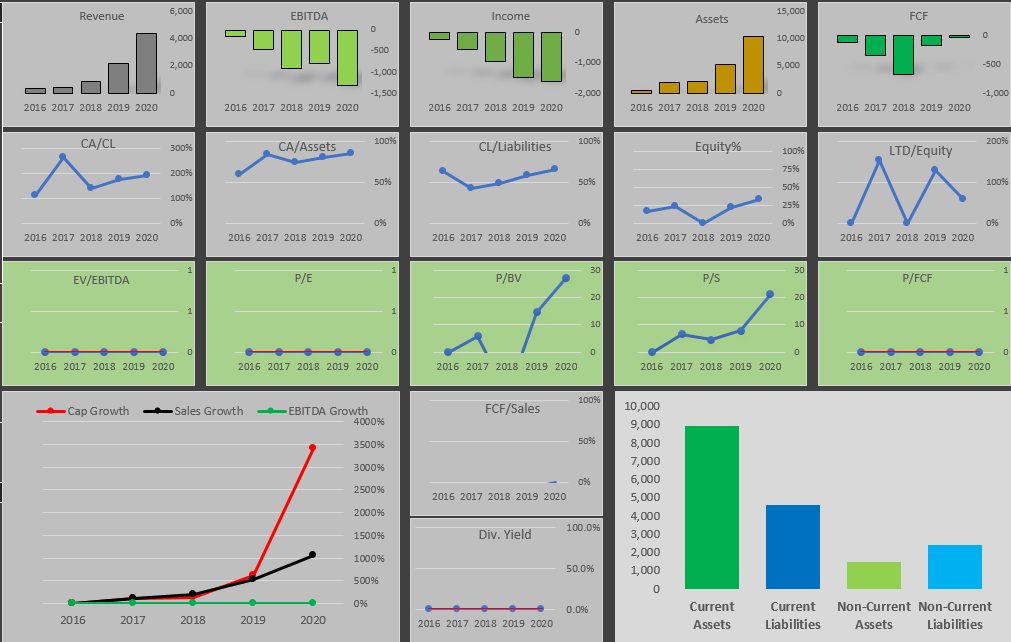

One of the most important metrics in growth companies like SE is a pace of the revenue growth. During the last 5 years SE has grown 89% annually and for the current fiscal year analysts predict that this pace will remain basically unchanged.

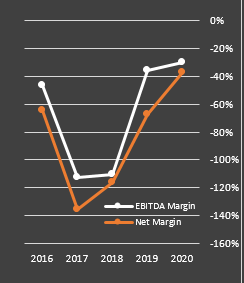

Both EBITDA and Income are negative, what is normal for the companies like SE. Although loss still grows in absolute numbers, margins are coming to break-even quickly and this shows that the company may soon become profitable. For now and in the next years SE will invest heavily in their high-growth profile and grabbing as big TAM as possible.

P.S. When it comes to TAM…

Company has a bit high leverage for me, however their Current Assets are covering all of the Liabilities easily, so it is not a problem at all.

They are not paying any dividend, which of course satisfies me, because the money is to stay in the company and be invested in its further development.

Stock/Valuation

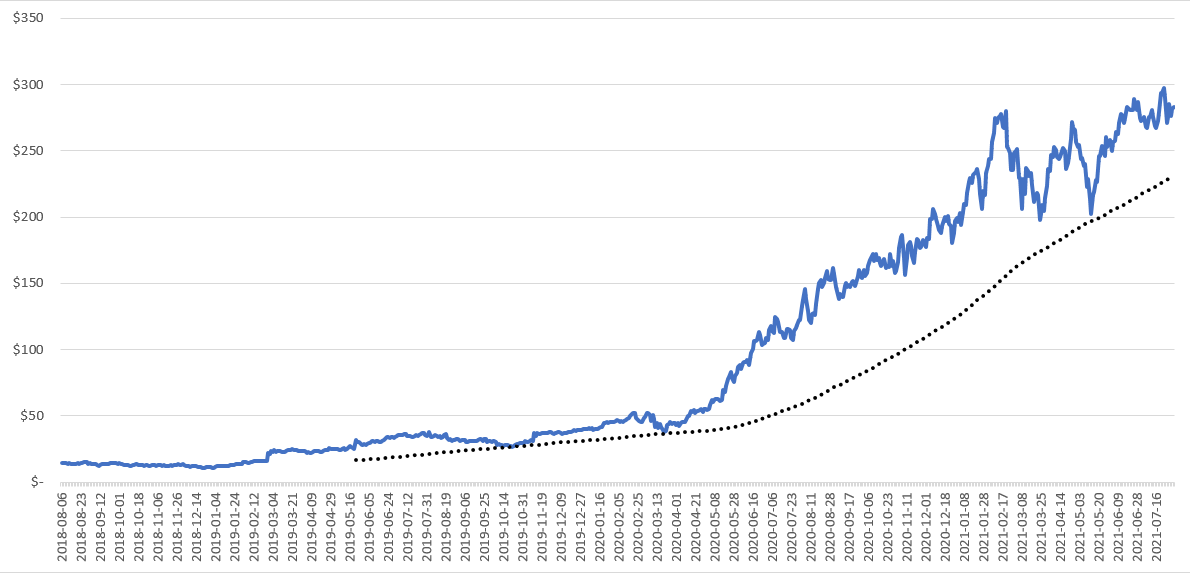

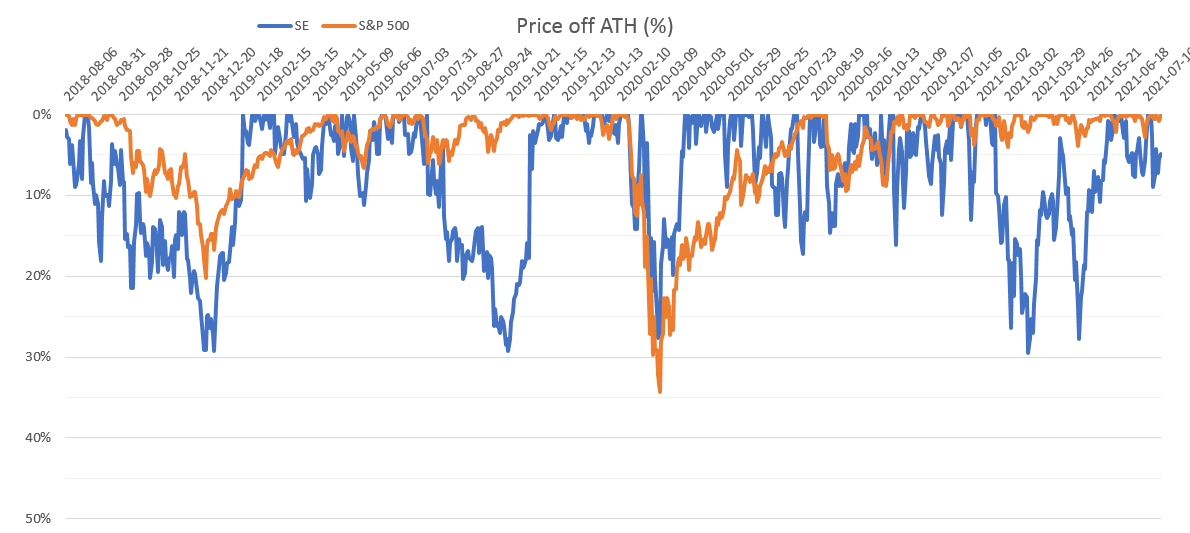

As befits a growth company, SEA is quite volatile, regularly going back 15-30% off high. However, since the COVID bottom it grew 744% (!) and they are going back from every correction very quickly (like during the coronavirus crash in March’20 - it returned from almost 30% correction to ATH much quicker than the market).

Of course, valuation is rich, with P/S over 20, which is significantly higher than in the previous year. But it is completely natural for high quality and high growth companies like that (actually, I prefer to buy expensive stocks, because they usually offer much more in their businesses - but relative valuation of course matters).

Summary

Sea Limited has become a unique combination of three different businesses, each offers high quality solutions. Their CEO and founder is really “skin-in-the-game” with his 25% stake. And the fact that Li is still in charge attracts me even more.

For me, every correction when price hits 200 MA (like in the middle of May’21 - shown in the chart above) will be a perfect time to buy the dip and increase my position.

For now, SE is in my favourite Top2 stocks (together with EVO) and I think that it will quickly become my biggest holding (it is not yet, because I care about portfolio correlation and I wasn’t sure if my stomach would take a bigger correction - but I think it is quite ok haha).

———————

Please let me know what do you think, any feedback will be much appreciated! That was my first post like that and I hope that it is at least readable :)